From Shaunda Devens, republished on 0xArchive. Read the original thread.

Pre-IPO perpetuals offer a market-based alternative to the fragmented IPO process, giving traders continuous price discovery and synthetic exposure to private companies that have historically restricted both participation and transparent valuation.

TradeXYZ’s Cerebras market offered an early validation of this structure. While the traditional IPO process remained gated, oversubscribed, and ultimately priced below where the public market cleared, TradeXYZ’s CBRS market had been tradable 24/7 since May 1, facilitating over $200M in pre-open volume with usable liquidity at a 62 bps median spread. As traditional reference points lagged, TradeXYZ consistently priced CBRS at a premium, and by the launch window its one-hour pre-print VWAP was only 1.2% above Nasdaq’s eventual $350 opening print.

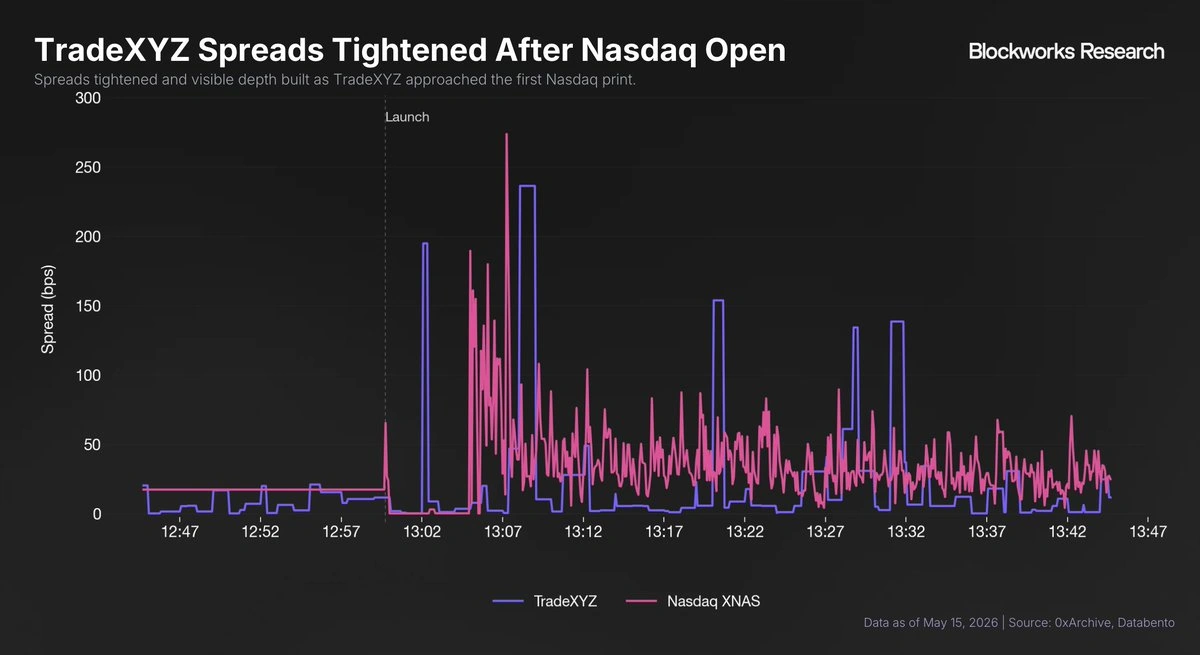

Liquidity also improved materially after the stock went live. Across the first 15 minutes following the Nasdaq print, TradeXYZ’s median spread compressed to 3.6 bps versus 27.7 bps on Nasdaq over the same window.

CBRS shows that pre-IPO perpetuals can serve as both an access product and a real-time information layer for markets that legacy infrastructure still prices through gated allocations and delayed public trading.

Analysis

TradeXYZ’s CBRS market launched on May 1 with a $175 reference price, already above the initial IPO range of $115-$125. At that stage, CBRS had no live equity anchor, so pricing was driven entirely by order-book demand and trader expectations of where the stock would clear two weeks later.

Traders continued to price CBRS well above the implied IPO value, with the contract trading at roughly a 100-200% premium to the indicated range. What initially looked aggressive became increasingly plausible as the IPO process evolved: the range was revised higher, the offering was upsized, and reported demand exceeded available shares by more than 20x.

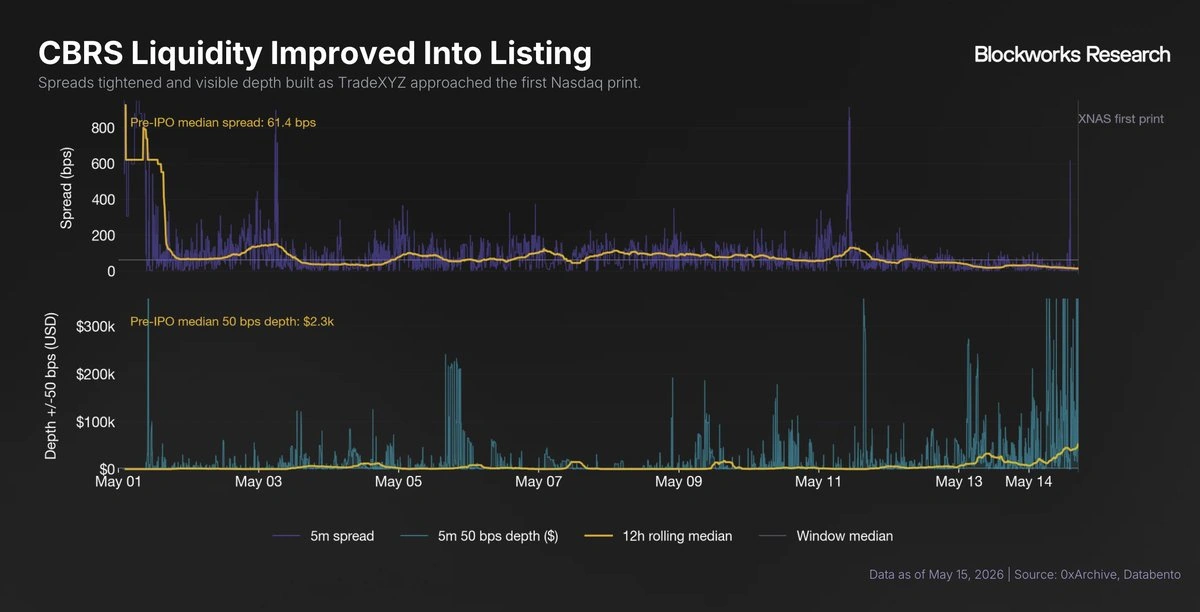

Liquidity was thin, but functional. With no liquid underlying asset to hedge against, median spreads were 61.4 bps, and median visible depth within 50 bps of mid was only $2.3k. Still, the alternative was not Nasdaq liquidity. Accessing CBRS through traditional secondaries would likely have involved 200-400 bps in explicit platform or broker fees, alongside transfer restrictions, minimum ticket sizes, delayed settlement, and potential SPV-level costs. TradeXYZ remained competitive, processing roughly $207M of notional volume before the first Nasdaq print.

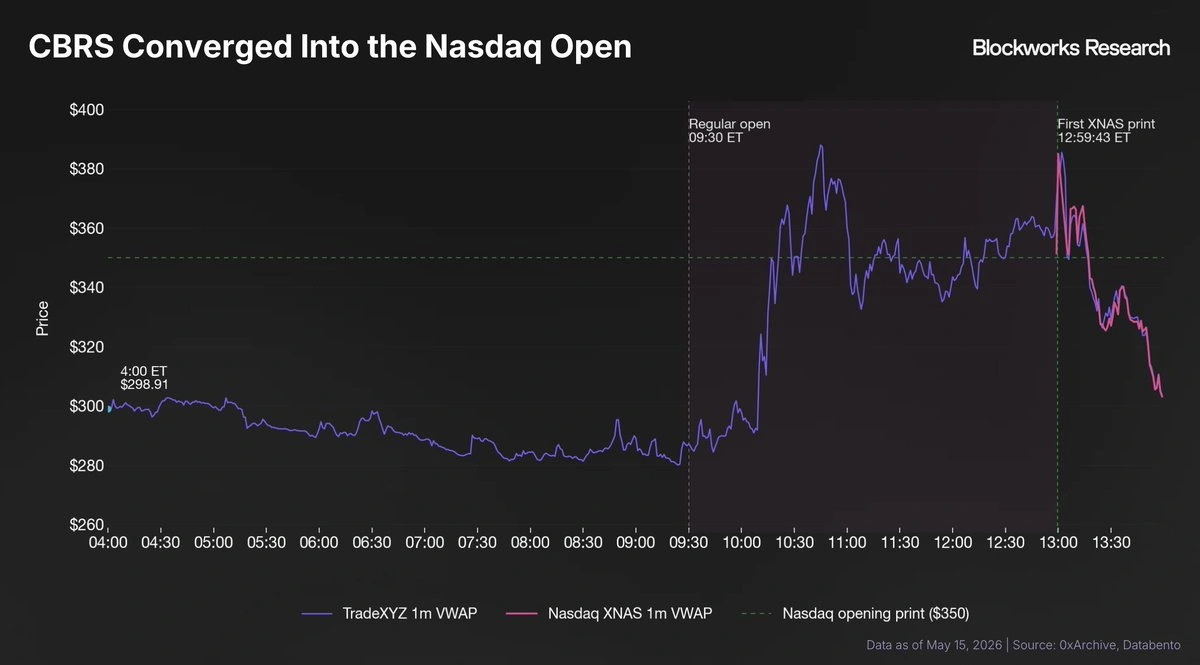

At 4:00 AM ET, Nasdaq’s NOII feed gave CBRS its first live external anchor through indicative cross data. If that signal had been materially away from TradeXYZ’s price, traders likely would have repriced the contract. Instead, the market stayed close, suggesting TradeXYZ had already converged toward the eventual public clearing level. It is also possible that TradeXYZ prices were being used as an additional reference by traders positioning around the open.

As Nasdaq’s indication process developed, TradeXYZ repriced from roughly $299 at 4:00 AM ET toward the eventual opening level. By the final minute before the XNAS cross, CBRS was trading around $360 on TradeXYZ, only 2.8% above Nasdaq’s $350 opening print. Across broader windows, the fit was even tighter: TradeXYZ’s one-hour pre-print VWAP was 1.2% above the open.

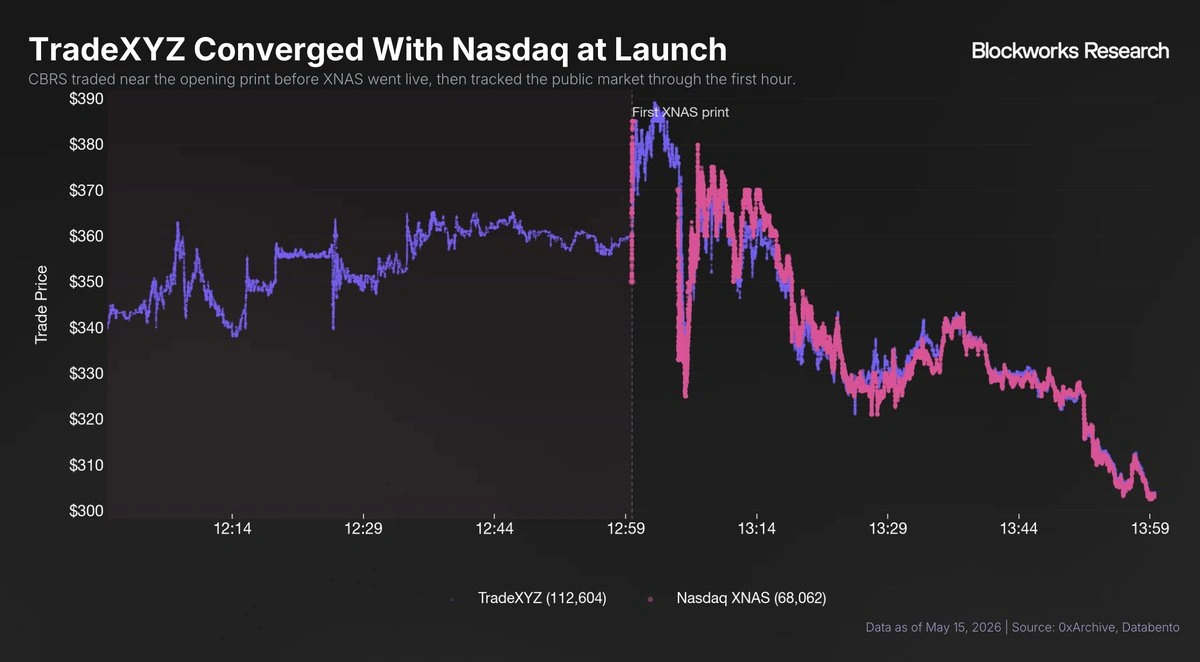

Following the open, TradeXYZ became materially more efficient. Spreads tightened from 11.7 bps ($0.42) in the final minute before the Nasdaq print to 2.0 bps ($0.07) in the first minute after XNAS went live, then held around 3.6 bps over the first 15 minutes post-print, versus 27.7 bps on Nasdaq over the same window.

Despite being TradeXYZ's first pre-IPO perpetual, CBRS already showed that the structure can be both efficient and informative: TradeXYZ’s market anticipated the Nasdaq open, carried meaningful signal into the listing, and tightened once the stock became hedgeable. If future high-profile private companies such as SpaceX, OpenAI, or Anthropic move toward public listings, TradeXYZ could become one of the first venues where market-based price discovery begins.

Credit: Shaunda Devens, originally published May 15, 2026. Original thread.