From Shaunda Devens, republished on 0xArchive. Read the original thread.

Key Findings

HIP-3 has scaled market creation, but not deployer competition. In 2026, external deployers have launched nearly all new markets, with Hyperliquid directly launching only 6 of 119. HIP-3 markets now account for $3.2B in open interest and roughly one-third of perpetual volume. However, activity has overwhelmingly concentrated around TradeXYZ, which controls 95%+ of HIP-3 volume and open interest.

Non-TradeXYZ deployers face structurally weak economics. With TradeXYZ dominating high-volume markets, other deployers are left competing for niche assets that are difficult to justify against the 500K HYPE bond and upfront auction costs. Most HIP-3 deployers generate returns near or below 1% on staked HYPE, while non-XYZ markets have a median auction-cost payback period of 4 years. TradeXYZ is the clear outlier, with an estimated 74% return on staked HYPE and a 5-month median auction-cost payback period.

Pressure on marginal deployers is already visible. Non-TradeXYZ deployers have launched only five paid markets since April, compared with 22 by TradeXYZ. Felix has become the first HIP-3 protocol to formally wind down, while Ventuals’ vHYPE has traded at a 20–30% discount to HYPE as holders seek early liquidity. If deployer economics remain unattractive, competition will only narrow further.

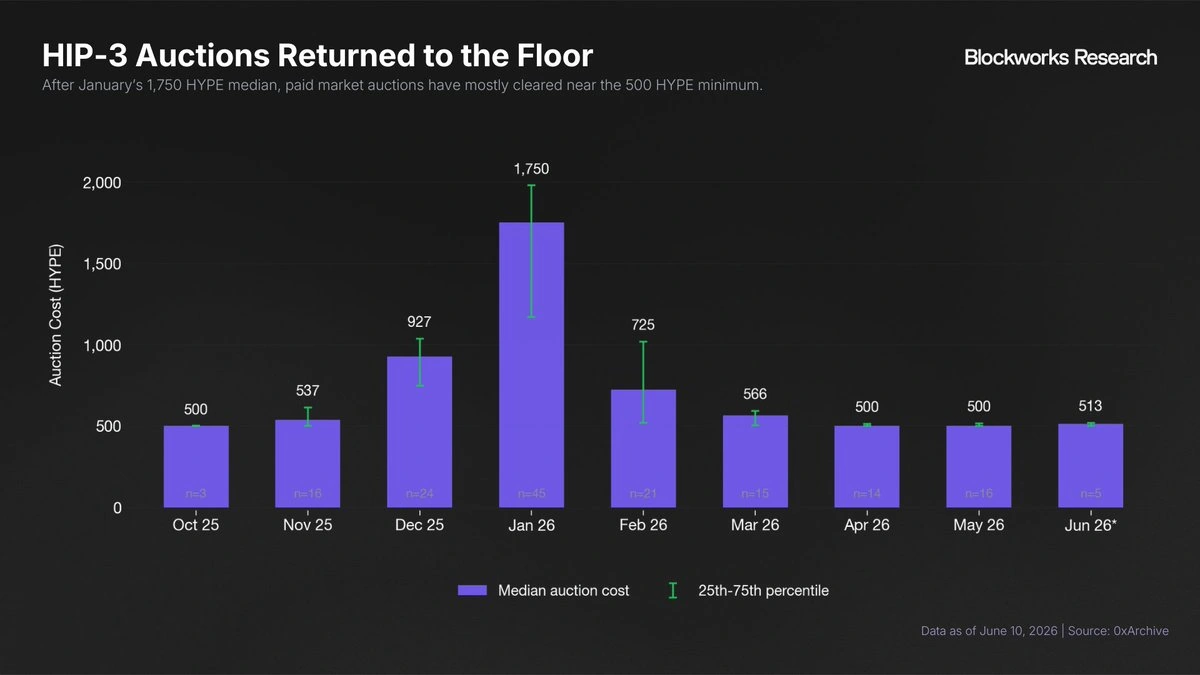

Deployer concentration introduces regulatory and structural risk. TradeXYZ has been instrumental to Hyperliquid’s growth, but concentrating high-demand listings in one deployer creates a clearer regulatory attack surface. More broadly, weak marginal-deployer economics reduce demand for new HIP-3 bonds and auction participation, with median paid listing prices falling from 1,750 HYPE in January to 500 HYPE in May. Under current incentives, HIP-3 is unlikely to sustain a competitive, decentralized listing market.

We propose two changes to support more sustainable market creation and HYPE value accrual. First, a tiered exchange model would allow deployers to launch with lower HYPE requirements but restricted permissions, including open interest caps, lower leverage, and tighter risk controls, before scaling up as they increase bonded HYPE. Second, auction economics could be adjusted so new markets can route up to 100% of fees to deployers until auction costs are recovered, or until the DEX reaches breakeven, before reverting to the standard split.

Introduction

HIP-3 has been central to Hyperliquid’s transition from a single exchange venue into a global liquidity infrastructure layer. By abstracting core exchange infrastructure, HIP-3 separates the exchange stack into three roles: HyperCore provides the underlying infrastructure, deployers list and operate new markets, and frontends route order flow through builder codes.

Through HIP-3, market creation has largely moved outside Hyperliquid itself: In 2026, only 6 of 119 new markets were launched by Hyperliquid, with the remainder coming from external deployers. These markets have generated $280.4B in cumulative volume, reached $3.2B in open interest, and now account for 29.3% of 30-day perpetual volume. HIP-3 has also enabled new products such as 24/7 equity-linked perps and pre-IPO markets like SpaceX, extending Hyperliquid beyond its original crypto-native market base.

However, this expansion also comes with additional risk. Unlike spot listings under HIP-1, perpetual markets introduce margin, oracle, mark price, liquidation, and bad debt risk. HIP-3 addresses this by requiring deployers to post a 500K HYPE stake, which functions as a slashable performance bond. Deployers can list markets permissionlessly but remain economically accountable through validator-enforced slashing.

Despite this, HIP-3 has not produced a competitive deployer market; TradeXYZ now accounts for over 95% of HIP-3 volume and OI, creating a self-reinforcing de facto monopoly in which new deployers are choked off by weak returns, limited differentiation, high stake requirements, and duplication risk. This report examines why that dominance emerged, why it is likely to persist, what it means for Hyperliquid’s market structure, and how HIP-3 could be adjusted to make market creation more competitive.

HIP-3 Deployer Competitive Landscape

Under HIP-3, deployers allocate HyperCore market slots toward markets with the highest expected demand and receive 50% of the revenue generated by the markets they operate. With core exchange infrastructure handled by HyperCore, deployer economics shift from traditional operating overhead to auction fees and the 500K HYPE stake, which functions primarily as a slashable performance bond but still carries opportunity cost, liquidity risk, and slashing exposure.

In theory, many deployers could compete across a broad set of markets. In practice, the highest-demand listings are obvious, particularly large-cap equities and commodities, while differentiation at the deployer layer remains limited. This has favored TradeXYZ, which had already built credibility through Unit’s handling of spot assets, gained an early advantage by listing USDC pairs while other deployers focused on USDH or USDT, and also benefits from user expectations that Unit could play a role in a potential S3 for Hyperliquid.

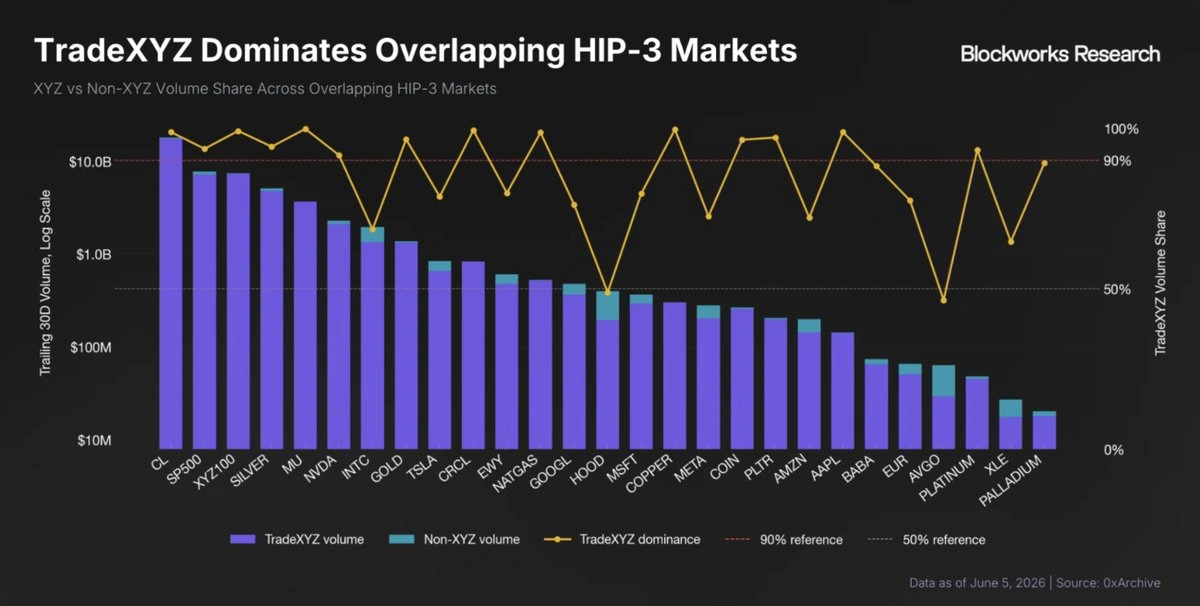

With no clear attack vector against this moat, non-TradeXYZ deployers are effectively choked off from high-demand markets. Even if a deployer identifies an attractive asset, sustained demand makes that market a target for TradeXYZ to duplicate, after which TradeXYZ can compete with stronger liquidity, trust, and existing user flow.

For example, Broadcom (AVGO) was listed through Nova’s MVP conviction market process and became one of the strongest non-XYZ listings, but after TradeXYZ launched its own AVGO market, volume shifted to the XYZ pair, which now does multiples of Nova’s volume. Overlapping HIP-3 markets show the same pattern, with duplicate listings overwhelmingly dominated by TradeXYZ pairs.

As a result, other deployers are pushed away from the most attractive markets and into narrower niches, such as Ventuals’ Semis basket or Paragon's BTC.D market. However, under a 500K HYPE bond, these opportunities are generally too small to justify the capital lockup, illiquidity, and slashing exposure.

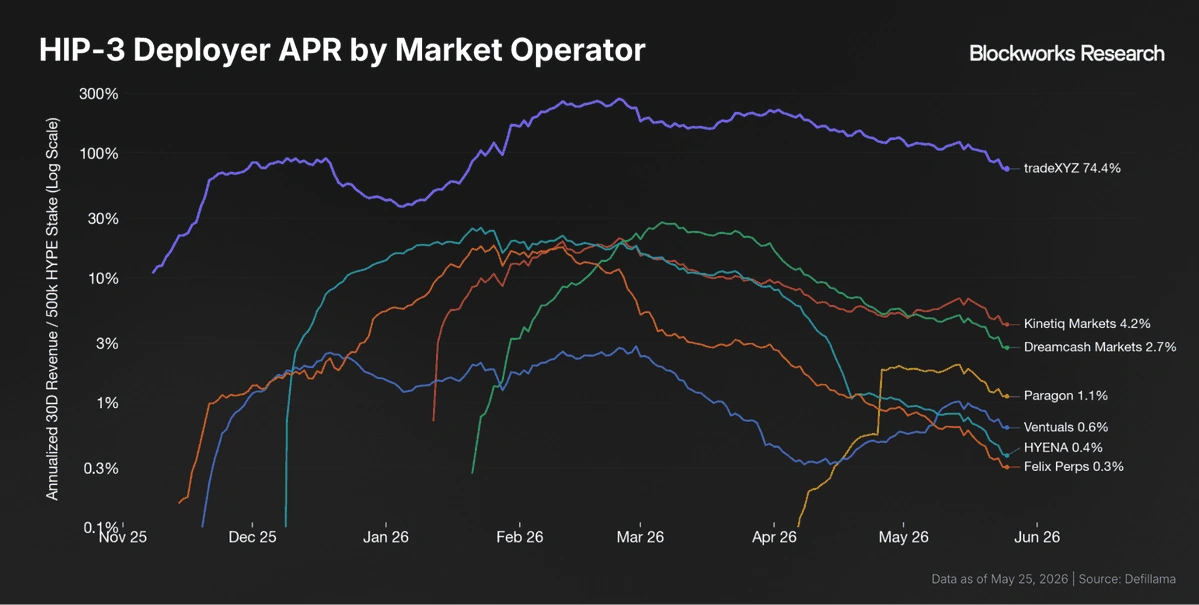

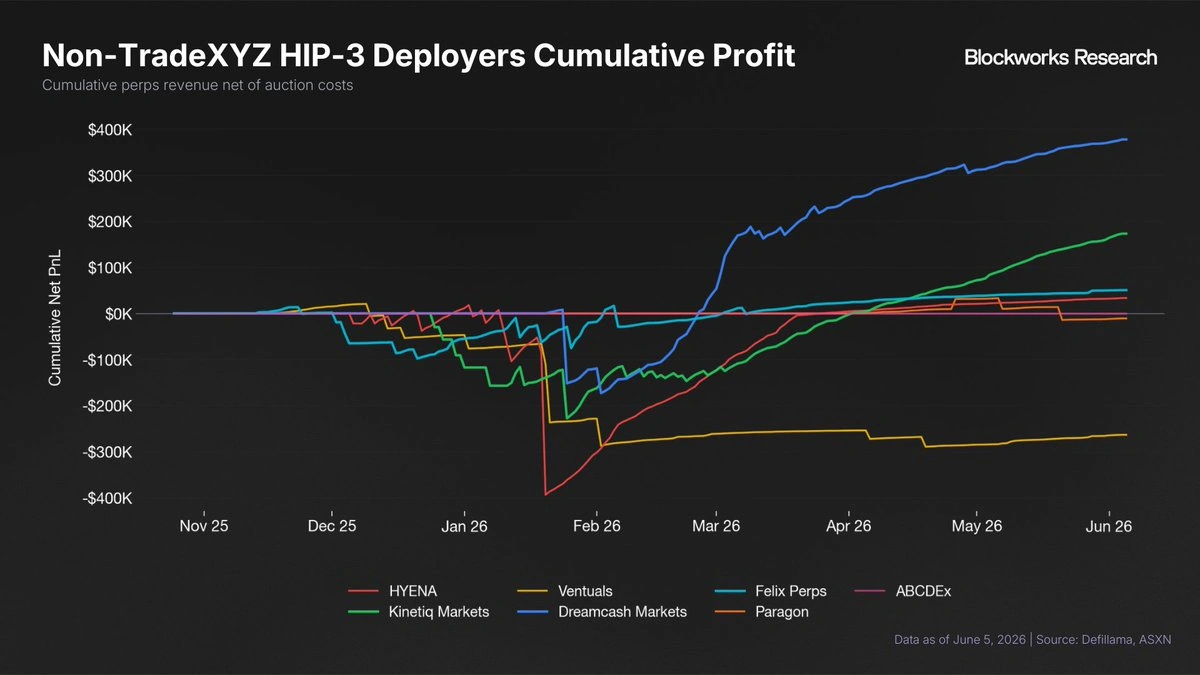

For example, if revenue is measured as a return on locked HYPE, only TradeXYZ appears to justify the liquidity risk, generating a 74% annualized return. Kinetiq and DreamCash trail far behind at 4.2% and 2.7%, while most other deployers are below 1%.

In practice, these figures still overstate what HYPE stakers actually earn. Deployers often source the required stake externally, either through third parties, as with Felix, or through crowdsourced deposits, as with Kinetiq and Ventuals. Stakers then receive only a share of deployer revenue; for example, kmHYPE holders receive just 10% of Kinetiq’s deployer revenue.

This makes already weak deployer returns even less attractive for underlying HYPE stakers, increasing withdrawal pressure and making it harder for marginal deployers to maintain the 500K HYPE bond. Felix is the first to formally exit, with Hyperion, the company that supplied its HYPE, stating it will reallocate the stake toward higher-yield opportunities. Other deployers could be next, such as Ventuals, where vHYPE trades at a 20–30% discount to HYPE as holders accept a haircut for early liquidity.

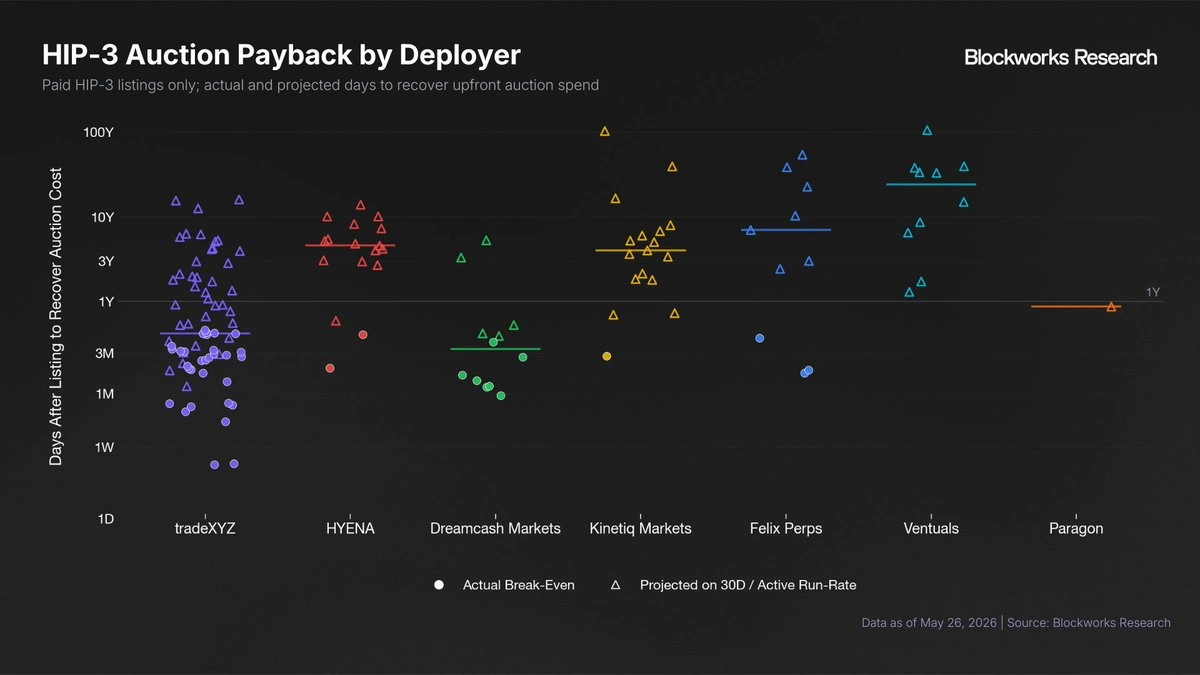

Still, the 500K HYPE bond is only one capital gate. The more direct cost is auction spend, which deployers must pay upfront for each new market. In our sample of 136 paid HIP-3 listings, only 44 have recovered their auction cost; the rest depend on projected payback using the latest 30-day fee run rate.

The median paid HIP-3 market takes 1.3 years to recover its auction cost, but the burden remains concentrated outside TradeXYZ. Non-XYZ markets have a median projected payback period of 4 years, versus 5 months for TradeXYZ. Auction spend therefore remains a second practical barrier to entry: even after sourcing the HYPE bond, non-XYZ deployers are often paying upfront for markets that may not become economically attractive for years.

At the DEX level, we see similar dynamics. Outside TradeXYZ, the few profitable deployers are largely those spending heavily on incentives and points. Even then, most deployers are barely breaking even on auction costs alone, before accounting for additional expenses such as market maker agreements, infrastructure, and other operating costs.

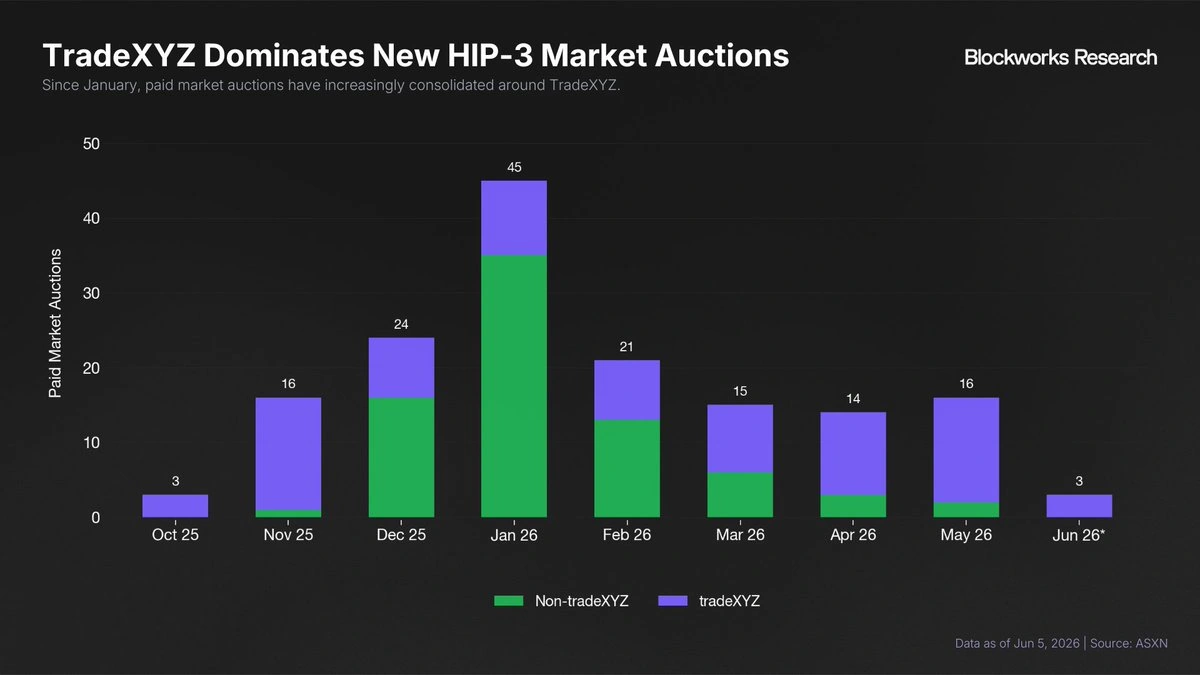

As a result, non-TradeXYZ auction activity has slowed sharply. Even among deployers that have already sourced the 500K HYPE bond, arguably the largest hurdle, additional markets appear difficult to justify. Since April, non-TradeXYZ teams have launched only five paid markets, compared with 22 by TradeXYZ.

Extrapolating forward, TradeXYZ is likely to continue dominating new HIP-3 listings. New deployers are priced out by weak expected returns, while existing deployers that have already crossed the staking hurdle are showing less willingness to commit additional auction capital. Without changes to HIP-3 incentives or market structure, TradeXYZ’s current dominance is likely to persist and deepen.

HIP-3 Deployer Dominance

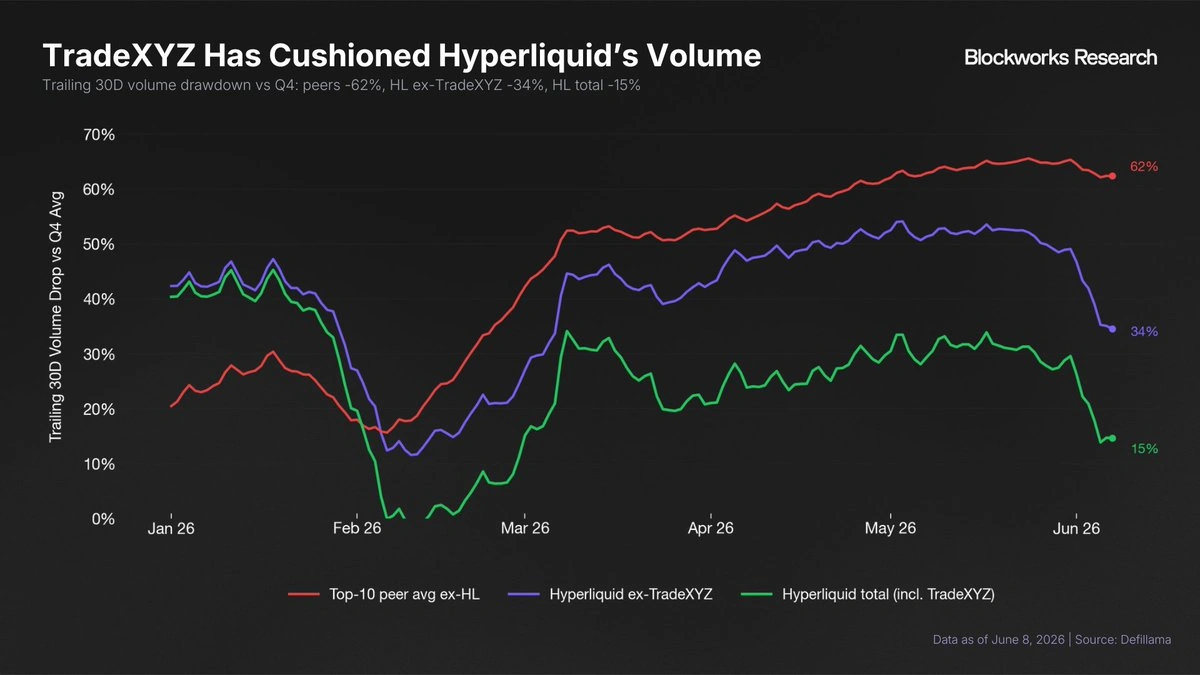

TradeXYZ’s dominance has not been harmful to Hyperliquid, however. If anything, it has been the main driver of Hyperliquid’s growth in 2026. TradeXYZ has executed HIP-3’s core function well: identifying high-demand markets, expanding Hyperliquid into equities, commodities, and pre-IPO products.

In an environment where crypto demand has been muted, TradeXYZ has helped Hyperliquid maintain volume share. On a trailing 30-day basis, the top-10 DEX peer average is down 62% versus Q4, while Hyperliquid excluding TradeXYZ is down 34%. Including TradeXYZ, Hyperliquid’s total volume is down only 15%, reflecting the contribution from real-world asset markets.

However, while TradeXYZ’s dominance has been earned and has been net positive for Hyperliquid’s growth, deployer-layer concentration introduces regulatory and structural risks.

The clearest is regulatory: Hyperliquid perps are not CFTC-compliant for US market access because they are not listed on, or operated through, a CFTC-registered Designated Contract Market. Equity and pre-IPO perps sharpen this further, as single-stock, ETF, narrow-index, or private-company-reference perps can fall into SEC security-based swap or joint SEC/CFTC security-futures territory. HIP-3 likely externalized market deployment to reduce Hyperliquid’s role as the sole listing authority, similar to how builder codes diversify frontend order flow. But if one entity lists most high-demand assets, listing accountability reconcentrates at the deployer layer, making it a more visible regulatory attack surface.

This concentration also weakens HIP-3’s economic flywheel. When one deployer captures most of the demand, expected returns for marginal deployers fall, making the 500K HYPE bond harder to justify. Recent behavior reflects this: Nova markets launched through Para’s existing HIP-3 deployer rather than standing up an independent bond. Fewer credible deployers also reduce auction competition, with the median paid listing price falling from 1,750 HYPE in January to 500 HYPE as TradeXYZ remains virtually the only consistent bidder.

Combined bond and auction costs also bias HIP-3 toward high-volume markets. This creates a risk that niche or differentiated assets become uneconomical, even when they are strategically valuable because they create net-new markets for users to trade, as Hyperps did early on. The result is less experimentation and a stronger incentive to focus on existing, proven markets.

More generally, the key point is that HIP-3’s current barriers appear too high to support a meaningfully decentralized market layer. If unchanged, listings are likely to remain concentrated around a single dominant entity, which could become more entrenched over time. We believe targeted adjustments to the HIP-3 model would benefit Hyperliquid over the long run by increasing HIP-3 market activity, improving auction participation, and supporting a more diverse base of deployers and markets.

Tiered HIP-3 Exchanges

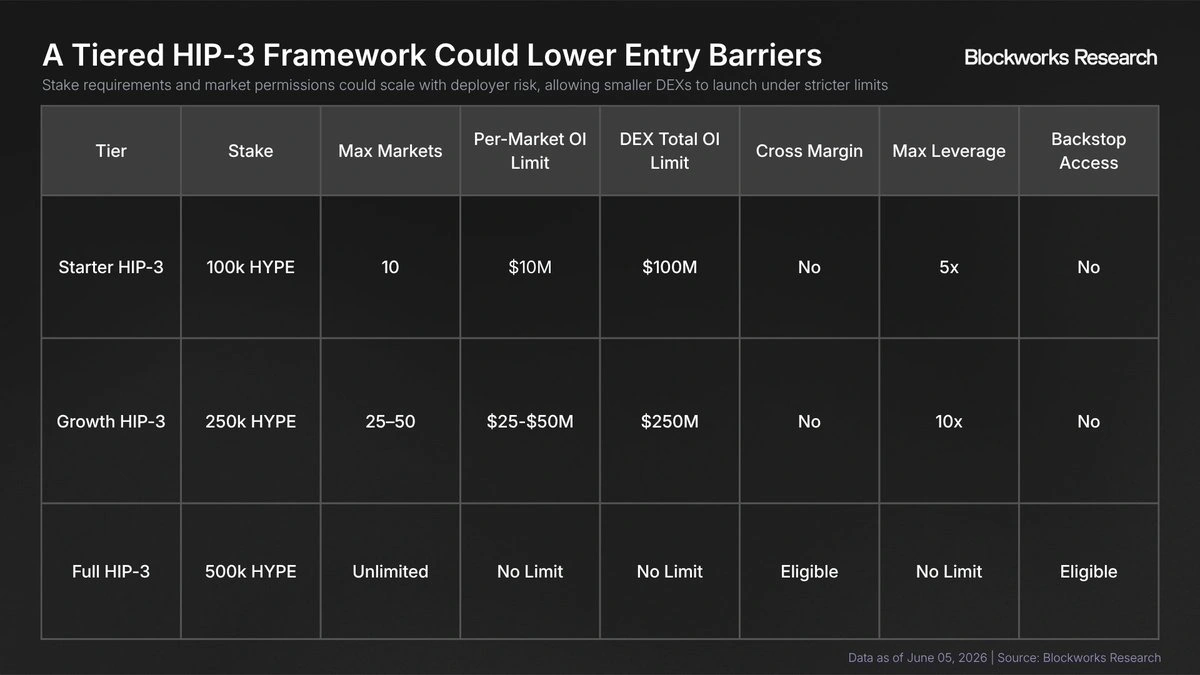

To increase listing and deployer diversity without weakening Hyperliquid’s security model, the clearest path forward is to reduce the HYPE stake requirement for smaller HIP-3 deployers. Hyperliquid already leaves room for this in its docs, stating that the 500k HYPE requirement is “expected to decrease over time as the infrastructure matures.”

To preserve protocol security and structural HYPE demand, Hyperliquid could introduce tiered HIP-3 exchanges. Today, all deployers face the same requirement because they receive broad permissions that can create protocol risk, including cross-margin access and backstop liquidation privileges. Smaller exchanges may not need these permissions. By limiting lower-tier deployers to more constrained risk parameters, Hyperliquid could reduce protocol risk and justify lower HYPE stake requirements.

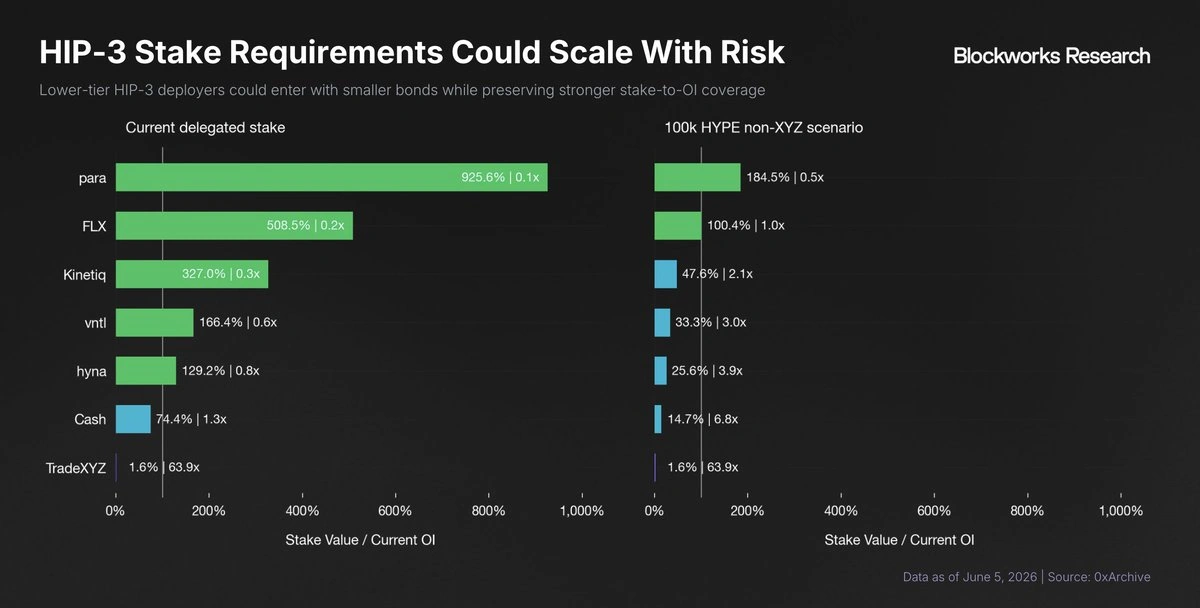

This is also supported by the risk profile of smaller deployers. These exchanges generally have lower open interest and less value at risk, meaning a smaller bond can still provide proportionate protection. For example, even if existing non-TradeXYZ deployers had their HYPE requirement reduced to 100K, they would still have over 10x greater OI-to-HYPE coverage than TradeXYZ.

An initial framework could use 100K, 250K, and 500K HYPE tiers, with permissions scaling by stake size. This would lower the barrier to entry while preserving HYPE demand, as deployers could start smaller, validate demand, and scale into higher tiers over time. It would also let a DEX wind down partially, delisting markets to drop into a lower tier, rather than shutting down entirely.

The key point is that disabling cross margin and backstop liquidation access materially contains risk. Even if a lower-tier deployer misconfigures a market or acts maliciously, losses should be isolated to that market or DEX, rather than creating broader protocol-level contagion.

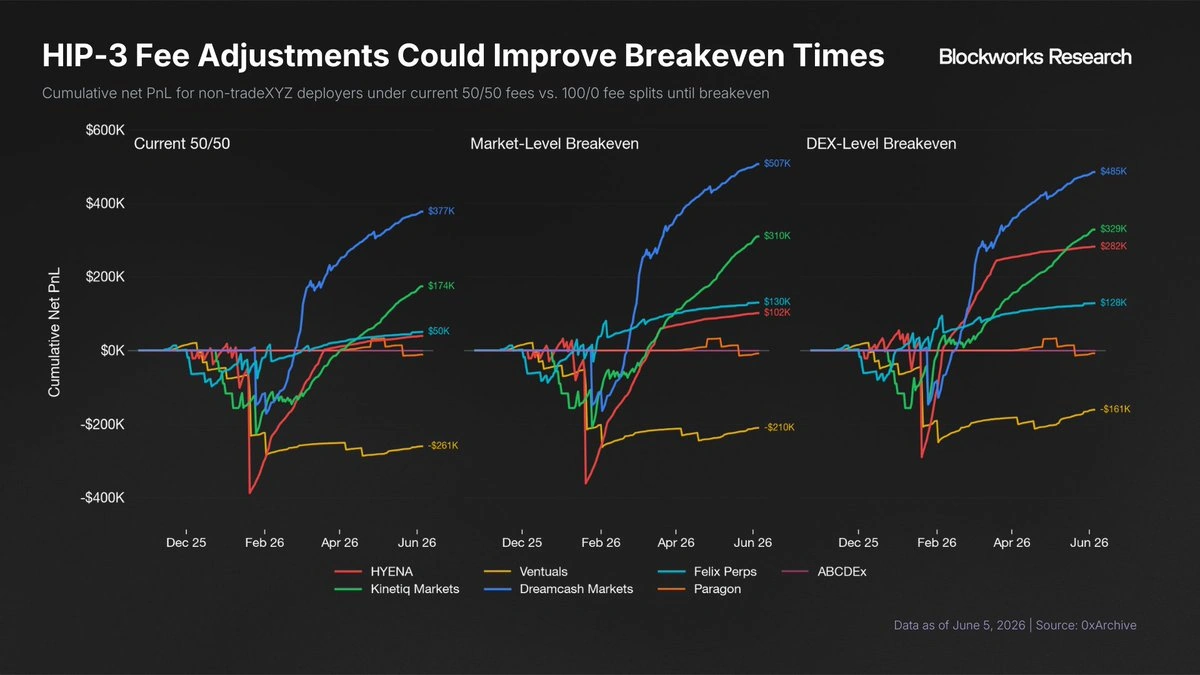

With tiered exchanges lowering barriers to deployer participation, auctions could also be adjusted to support more active market listings. One approach is to temporarily shift the fee split for newly auctioned markets from 50/50 deployer/protocol to 100/0 until the deployer recoups its auction cost, after which fees would revert to the standard 50/50 model.

A more aggressive version would add a DEX-level component on top of this. A deployer would still earn 100% of fees on any individual market that hasn't yet broken even, but it would also earn 100% across all markets, including those already profitable, whenever the DEX's cumulative auction spend exceeds its lifetime revenue. The split reverts to 50/50 once total revenue surpasses total auction cost.

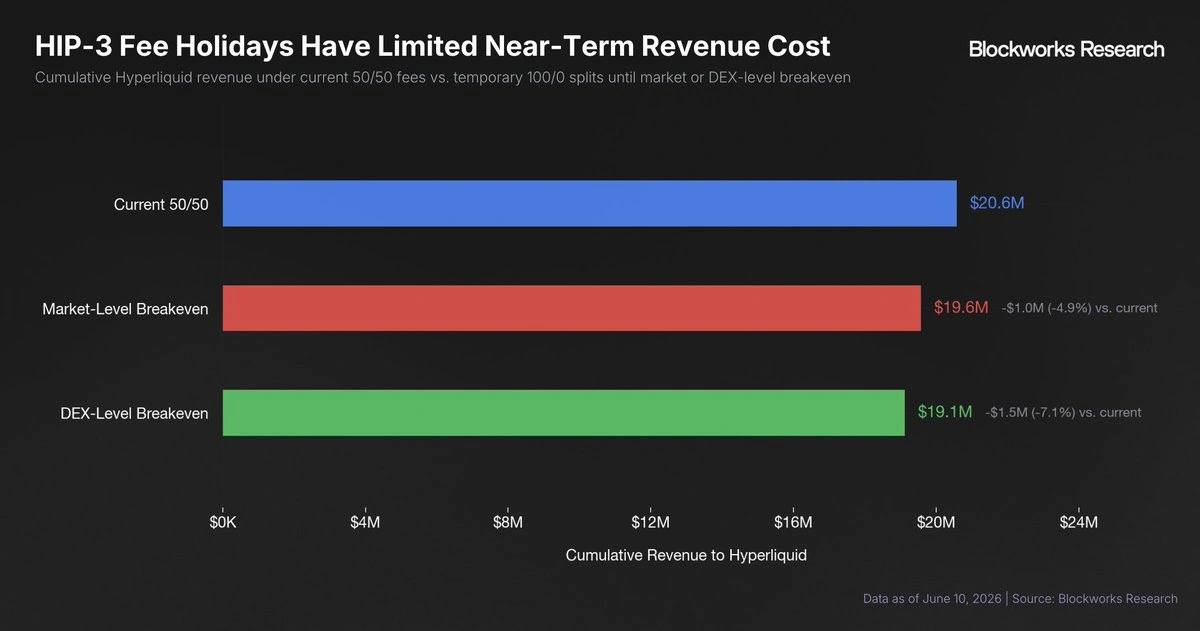

This might seem too aggressive, but pre-breakeven markets generate only a small share of HIP-3 revenue compared to mature, successful ones, so redirecting their fees to deployers would cost Hyperliquid little in the near term.

In exchange, deployers receive a stronger incentive to keep listing and testing new markets. If those markets succeed, Hyperliquid still earns the standard 50/50 split after breakeven while benefiting from a broader market surface. Under the more aggressive DEX-level model, deployers are further incentivized to recycle revenue into additional auctions, creating a flywheel of more listings, more HYPE demand, and ultimately greater long-term protocol revenue.

Overall, we believe tiered staking and temporary auction-fee relief would lower barriers to entry without abandoning Hyperliquid’s security model. Smaller deployers could launch under tighter risk limits, prove demand, and scale into higher tiers over time, while auction recoupment would make continued market experimentation more economically viable. The result is a broader deployer base, more active market creation, and sustained demand for HYPE both as a bond and for auctions.

Conclusion

While HIP-3 has been extremely successful at generating volume, it has done far less to decentralize market creation across deployers. Several headwinds have turned auctions and bonded HYPE into real barriers to entry: USDH depreciation, fee compression from growth mode, and HYPE appreciation driving up the cost of the 500K stake. Together, these also limit existing deployers' ability to list additional markets. With Felix winding down, pressure on Ventuals, and Coinbase's acquisition of the USDH brand IP forcing USDH-denominated teams to settle and relist their markets in USDC, the next few months will determine whether HIP-3 becomes a diversified, competitive market layer or prices out all but the dominant deployers.

We believe tiered staking and temporary auction-fee relief offer a practical path forward. Lower-risk deployers could launch under stricter limits, while fee relief would make niche markets more viable in an environment where bidding appetite has weakened. Over time, more listings, broader deployer participation, and recycled auction activity should strengthen the HIP-3 flywheel, improve market diversity, and support long-term demand for staked HYPE.

The information contained in this report and by Blockworks Inc. and related affiliates is for general informational purposes only and is not intended to provide legal, financial, or investment advice. The report should not be construed as an offer or solicitation to buy or sell any security, token, or financial instrument and does not represent any recommendation or endorsement of any investment or financial product or service. Blockworks Inc. and related affiliates are not registered as a securities broker-dealer or an investment advisor in any jurisdiction or country.

Credit: Shaunda Devens, originally published June 11, 2026. Original thread.